NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

36Attachment DD – Rules to Allocate the Cost of NY Transco LLC Transmission Facilities and Formula Rates

36.1Overview

36.1.1Cost Allocation

The purpose of Section 36.2 is to provide for the allocation of costs to be recovered through the Transco Facilities Charge (“TFC”) described in Section 6.13 of Schedule 13 of the ISO OATT for the following NY Transco, LLC (“NY Transco”) projects: (1) the Second Ramapo-to-Rock Tavern 345-kV Line Project, the Marcy South Series Compensation and Fraser-to-Coopers Corners Reconductoring Project, and the Staten Island Unbottling Project, each of which have been approved by the New York Public Service Commission on November 4, 2013, in Case No. 12-E-0503 (the “Transmission Owner Transmission Solutions” or “TOTS” projects); (2) the Second Oakdale-to-Fraser 345-kV Line Project and the Edic-to-Pleasant Valley 345-kV Line Project (the “AC” projects) upon approval by the New York Public Service Commission in Case Number 12-T-502 and subject to inclusion by the ISO in the ISO transmission plan for purposes of cost allocation; and (3) any regulated public policy transmission project that has been approved by the ISO pursuant to Section 31.4.8 of Attachment Y of the ISO OATT and determined to be eligible to recover such costs pursuant to Sections 31.5.5.3 and 31.5.5.4 of Attachment Y of the ISO OATT. Section 36.2 shall include cost allocation tables for each NY Transco project eligible to recover costs through the TFC.

36.1.2Formula Rates

Section 36.3 provides NY Transco’s formula rate and implementation rules for the formula rate to recover costs related to its projects through the TFC.

36.2Attachment 1 to Attachment DD

36.2.1Allocation Tables

36.2.1.1.Second Ramapo-to-Rock Tavern 345-kV Line Project

COST ALLOCATION TABLE FOR THE SECOND RAMAPO-TO-ROCK TAVERN 345-KV LINE PROJECT |

Transmission District | Allocation of Project Costs (%)[1] |

Consolidated Edison Co. of NY, Inc. Orange and Rockland Utilities, Inc. | 41.7 |

New York Power Authority | 16.9 |

Long Island Power Authority | 16.7 |

Niagara Mohawk Power Corp. | 10.4 |

New York Gas & Electric Corp. Rochester Gas and Electric Corp. | 8.9 |

Central Hudson Gas & Electric Corp. | 5.4 |

| |

36.2.1.2Marcy South Series Compensation and Fraser-to-Coopers Corners Reconductoring Project

COST ALLOCATION TABLE FOR THE MARCY SOUTH SERIES COMPENSATION AND FRASER-TO-COOPERS CORNERS RECONDUCTORING PROJECT |

Transmission District | Allocation of Project Costs (%)[2] |

Consolidated Edison Co. of NY, Inc. Orange and Rockland Utilities, Inc. | 41.7 |

New York Power Authority | 16.9 |

Long Island Power Authority | 16.7 |

Niagara Mohawk Power Corp. | 10.4 |

New York Gas & Electric Corp. Rochester Gas and Electric Corp. | 8.9 |

Central Hudson Gas & Electric Corp. | 5.4 |

| |

36.2.1.3Staten Island Unbottling Project

COST ALLOCATION TABLE FOR THE STATEN ISLAND UNBOTTLING PROJECT |

Transmission District | Allocation of Project Costs (%)[3] |

Consolidated Edison Co. of NY, Inc. Orange and Rockland Utilities, Inc. | 41.7 |

New York Power Authority | 16.9 |

Long Island Power Authority | 16.7 |

Niagara Mohawk Power Corp. | 10.4 |

New York Gas & Electric Corp. Rochester Gas and Electric Corp. | 8.9 |

Central Hudson Gas & Electric Corp. | 5.4 |

| |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

36.3Attachment 2 to Attachment DD

36.3.1Formula Rates

36.3.1.1Rate Formula Template

Appendix A Page 1 of 5

Formula Rate - Non-LevelizedRate Formula Template

Utilizing FERC Form 1 DataProjected Annual Transmission Revenue Requirement

For the 12 months ended 12/31/

New York Transco LLC

(1)(2)(3) Line Allocated

No.Amount

1GROSS REVENUE REQUIREMENT(line 74)12 months$-

| REVENUE CREDITS | | Total | | Allocator | |

2 | Total Revenue Credits | Attachment 1, line 6 | | -TP | | -- |

3 | Net Revenue Requirement | (line 1 minus line 2) | | | | - |

4 | True-up Adjustment | Attachment 7 | | -DA | | -- |

5 | NET ADJUSTED REVENUE REQUIREMENT | (line 3 plus line 4) | | | | $- |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Appendix A Page 2 of 5

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Formula Rate - Non-LevelizedRate Formula Template

Utilizing FERC Form 1 Data

New York Transco LLC

(1)(2)(3)(4)(5)

Form No. 1 Transmission Line Page, Line, Col. Company Total Allocator (Col 3 times Col 4) No. RATE BASE:

For the 12 months ended 12/31/

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

| GROSS PLANT IN SERVICE (Note M) | |

6 | Production | (Attach 2, line 75) | -NA | -- |

7 | Transmission | (Attach 2, line 15) | -TP | -- |

8 | Distribution | (Attach 2, line 30) | -NA | -- |

9 | General & Intangible | (Attach 2, lines 45 & 60) | -W/S | -- |

10 | TOTAL GROSS PLANT (sum lines 6-9) | (GP=1 if plant =0) | -GP= | -- |

| | | | |

11ACCUMULATED DEPRECIATION & AMORTIZATION (Note M)

12 | Production | (Attach 2, line 151) | -NA | -- |

13 | Transmission | (Attach 2, line 91) | -TP | -- |

14 | Distribution | (Attach 2, line 106) | -NA | -- |

15 | General & Intangible | (Attach 2, lines 121 & 136 | -W/S | -- |

16TOTAL ACCUM. DEPRECIATION (sum lines 12-15)-- |

17 | NET PLANT IN SERVICE | | | |

18 | Production | (line 6- line 12) | - | - |

19 | Transmission | (line 7- line 13) | - | - |

20 | Distribution | (line 8- line 14) | - | - |

21 | General & Intangible | (line 9- line 15) | - | - |

22 | TOTAL NET PLANT (sum lines 18-21) | (NP=1 if plant =0) | -NP= | -- |

23 | ADJUSTMENTS TO RATE BASE(Note A) | | | |

24 | ADIT | (Attach 6a, line 9) | -TP | -- |

25 | Account No. 255 (enter negative) (Note F) | (Attach 3, line 153) | -NP | -- |

26 | CWIP | (Attach 3, line 185) (Note J) | -DA | - |

27 | Unfunded Reserves (enter negative) | (Attach 3, line 187) | -DA | -- |

28 | Unamortized Regulatory Assets | (Attach 3, line 212) (Note L) | -DA | -- |

29 | Unamortized Abandoned Plant | (Attach 3, line 154) (Note K) | -DA | -- |

30 | TOTAL ADJUSTMENTS (sum lines 24-29) | | - | - |

31 | LAND HELD FOR FUTURE USE | (Attach 3, line 186) | -TP | -- |

32 | WORKING CAPITAL (Note C) | | | |

33 | CWC | calculated (1/8 * Line 44) | - | - |

34 | Materials & Supplies (Note B) | (Attach 3, line 206) | -TP | -- |

35 | Prepayments (Account 165 - Note C) | (Attach 3, line 170) | -GP | -- |

36 | TOTAL WORKING CAPITAL (sum lines 33-35) | | - | - |

37 | RATE BASE (sum lines 22, 30, 31, & 36) | | - | - |

| | | | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Appendix A Page 3 of 5

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Formula Rate - Non-LevelizedRate Formula Template

Utilizing FERC Form 1 Data

New York Transco LLC

(1)(2)(3)(4)(5)

Form No. 1Transmission

Page, Line, Col.Company TotalAllocator(Col 3 times Col 4)

38O&M

39Transmission321.112.b-TP=--

For the 12 months ended 12/31/

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

40 | Less Accounts 565, 561 and 561.1 to 561.8 | 321.96.b & 84.b to 92.b | -TP= | | -- |

41 | A&G | 323.197.b | -W/S | | -- |

42 | Less EPRI & Reg. Comm. Exp. & Other Ad. | (Note D & Attach 3, line 189) | -DA | | -- |

43 | Plus Transmission Related Reg. Comm. Exp. | (Note D & Attach 3, line 189) | -TP= | | -- |

44 | PBOP expense adjustment | (Attach 3, line 292) | -TP= | | -- |

44a | Less Account 566 | 323.97.b | -DA | | -- |

44b 44c 45 | Amortization of Regulatory Assets Account 566 excluding amort. of Reg Assets TOTAL O&M (sum lines 39, 41, 43, 44, 44b, 44c | (Attach 3, line 210a) (line 44a less line 44b) less lines 40 & 42, 44a) (Note D) | -DA -DA - | | -- -- - |

46 | DEPRECIATION EXPENSE (Note M) | | | | |

47 | Transmission | 336.7.b & c | -TP | | -- |

48 | General and Intangible | 336.1.d&e + 336.10.b&c | -W/S | | -- |

49 | Amortization of Abandoned Plant | (Attach 3, line 155) (Note K) | -DA | | -- |

50 | TOTAL DEPRECIATION (Sum lines 47-49) | | - | | - |

51 | TAXES OTHER THAN INCOME TAXES (Note E) | | | | |

52 | LABOR RELATED | | | | |

53 | Payroll | 263._.i (enter FN1 line #) | -W/S | | -- |

54 55 | Highway and vehicle PLANT RELATED | 263._.i (enter FN1 line #) | -W/S | | -- |

56 | Property | 263._.i (enter FN1 line #) | -GP | | -- |

57 | Gross Receipts | 263._.i (enter FN1 line #) | -NA | | -- |

58 | Other | 263._.i (enter FN1 line #) | -GP | | -- |

59 | TOTAL OTHER TAXES (sum lines 53-58) | | - | | - |

60 | INCOME TAXES | (Note F) | | | |

61 | T=1 - {[(1 - SIT) * (1 - FIT)] / (1 - SIT * FIT * p))}*(1-n) = | - | | |

62 | CIT=(T/1-T) * (1-(WCLTD/R)) = | - | | |

63 | where WCLTD=(line 91) and R= (line 94) | | | |

64 | and FIT, SIT, p, & n are as given in footnote F. | | | |

65 | 1 / (1 - T) = (T from line 61) | - | | |

66 | Amortized Investment Tax Credit (266.8f) (enter negative) | - | | |

67 | Income Tax Calculation = line 62 * line 71 * (1-n) | - | | - |

68 | ITC adjustment (line 65 * line 66 * (1- n)) | -NP | | -- |

69Total Income Taxes(line 67 plus line 68)-- |

70 | RETURN | | | |

71 | [ Rate Base (line 37) * Rate of Return (line 94)] | -NA | | - |

72 | Rev Requirement before Incentive Projects (sum lines 45, 50, 59, 69, 71) | - | | - |

73 | Incentive Return and Income Tax on Authorized Projects (Attach 4, line 58, col h) | -DA | 100% | - |

74 | Total Revenue Requirement (sum lines 72 & 73) | - | | - |

| | | | | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Appendix A Page 4 of 5

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Formula Rate - Non-LevelizedRate Formula Template

Utilizing FERC Form 1 Data

New York Transco LLC SUPPORTING CALCULATIONS AND NOTES

75TRANSMISSION PLANT INCLUDED IN RTO RATES

76Total transmission plant (line 7, column 3)-

77Less transmission plant excluded from RTO rates(Note H)-

78Less transmission plant included in OATT Ancillary Services (Note H)-

79Transmission plant included in RTO rates (line 76 less lines 77 & 78)-

80Percentage of transmission plant included in RTO Rates (line 79 divided by line 76)TP=-

For the 12 months ended 12/31/

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

81WAGES & SALARY ALLOCATOR (W&S) (Note I)

82Form 1 Reference$TPAllocation

83Production

84Transmission-

85Distribution

86Other

W&S Allocator

($ / Allocation)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

87Total (sum lines 83-86) [WS equals 1 if there are no wages & salaries]--=-=WS

88RETURN (R) (Note J)

89

90$%CostWeighted

91 | Long Term Debt | (Attachments 3 and 5) (Note G) | --- | | -=WCLTD |

92 | Preferred Stock | (Attach 3, line 235 - 237) | --- | | - |

93 | Common Stock | (Attach 3, line 227) | --10.60% | | - |

94 | Total (sum lines 91-93) | | - | | -=R |

Sum Of Net Plant, CWIP, Regulatory Asset and Abandoned Plant | (a) | (b) | | (c) |

| Non-incentive Projects | Incenitve Projects | Total | |

95 | Net Transmission Plant in Service | (Line 19) | --- |

96 | CWIP in Rate Base | (Line 26) | --- |

97 | Unamortized Abandoned Plant | (Line 29) | -- |

98 | Regulatory Assets | (Line 28) | -- |

| | | | | | |

99Sum Of Net Plant, CWIP, Regulatory Asset and Abandoned Plant---

100 | Rev Requirement before Incentive Projects | (Line 72) | - |

101 | Total Revenue Credits | (Line 2) | - |

102 | Base Carrying Charge | (Line 100 - Line 101)/ Line 99 | - |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Note

Letter

SUPPORTING CALCULATIONS AND NOTES

Formula Rate - Non-LevelizedRate Formula Template

Utilizing FERC Form 1 Data

New York Transco LLC

General Note: References to pages in this formulary rate are indicated as: (page#, line#, col.#) References to data from FERC Form 1 are indicated as: #.y.x (page, line, column)

Appendix A Page 5 of 5

For the 12 months ended 12/31/

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

AThe balances in Accounts 190, 281, 282 and 283, as adjusted by any amounts in contra accounts identified as regulatory assets or liabilities related to FASB 106 or 109. Balance of Account 255 is reduced by prior flow throughs and excluded if the utility chose to utilize amortization of tax credits against taxable income as discussed in Note F. Account 281 is not allocated.

BIdentified in Form 1 as being only transmission related.

CCash Working Capital assigned to transmission is one-eighth of O&M allocated to transmission

Prepayments are the electric related prepayments booked to Account No. 165 and reported on Pages 110-111 line 57 in the Form 1.

DLine 41 removes EPRI Annual Membership Dues listed in Form 1 at 353._.f (enter FN1 line #),

any EPRI Lobbying expenses included in line 44 of the template and all Regulatory Commission Expenses itemized at 351.h

Line 41 removes all advertising included in Account 930.1, except safety, education or out-reach related advertising

Line 41 removes EEI and EPRI research, development and demonstration expenses associated with projects in which transmission customers can voluntarily participate to the extent such expenses exceed a maximum annual aggregate amount of $100,000

Line 42 reflects all Regulatory Commission Expenses directly related to transmission service, RTO filings, or transmission siting itemized at 351.h

Line 38 or Line 41 and thus Line 45 shall include any NYISO charges other than penalties, including but not limited to administrative costs.

EIncludes only FICA, unemployment, highway, property, gross receipts, and other assessments charged in the current year.

Taxes related to income are excluded. Gross receipts taxes are not included in transmission revenue requirement in the Rate Formula Template, since they are recovered elsewhere.

FThe currently effective income tax rate, where FIT is the Federal income tax rate; SIT is the State income tax rate, and p =

"the percentage of federal income tax deductible for state income taxes". If the utility is taxed in more than one state it must attach a work paper showing the name of each state and how the blended or composite SIT was developed. Furthermore, a utility that elected to utilize amortization of tax credits against taxable income, rather than book tax credits to Account No. 255 and reduce

rate base.

multiplied by (1/1-T) .

Inputs Required:FIT =-

SIT=-(State Income Tax Rate or Composite SIT from Attach 3)

p =-(percent of federal income tax deductible for state purposes)

n=-(not for profit entity ownership percentage)

For each Rate Year (including both Annual Projections and True-Up Adjustments) the statutory income tax rates utilized in the Formula Rate shall reflect the weighted average rates

actually in effect during the Rate Year. For example, if the statutory tax rate is 10% from January 1 through June 30, and 5% from July 1 through December 31, such rates would be weighted

181/365 and 184/365, respectively, for a non-leap year.

GThe cost of debt is determined using the internal rate of return methodology shown on Attachment 5 once project financing is obtained. Prior to obtaining project financing,

the interest rate in Table 2 of Attachment 5 will be used and will not be trued up. Attachment 5 contains an estimate of the internal rate of return methodology; the methodology will be applied to actual amounts for use in Appendix A.

After January 1, 2019 or the completion of construction, which ever occurs earlier, the cost of debt will be calculated pursuant to Attachment 3

HRemoves dollar amount of transmission plant included in the development of OATT ancillary services rates and generation step-up facilities, which are deemed to be included in OATT ancillary services. For these purposes, generation step-up facilities are those facilities at a generator substation on which there is no through-flow when the generator is shut down.

IEnter dollar amounts

JROE will be supported in the original filing and no change in ROE may be made absent a filing with FERC under FPA Section 205 or 206.

The capital structure will be 60% equity and 40% debt for the CWIP associated with the projects and Regulatory Assets in line 28, and the return on such projects will be input on line 71. The CWIP Projects will not be included in rate base (line 25). The capital structure shown on lines 89-92 will be 60% equity and 40% debt until January 1, 2019 or the completion of construction, which ever occurs earlier. After January 1, 2019 or the completion of construction, which ever occurs earlier, the capital structure on lines 89-92 will reflect the actual capital structure, and will be capped at 60% equity. If the actual equity ratio exceeds 60%, the common stock ratio will be reset to 60% and the debt ratio will be equal to 1 minus sum of the preferred stock ratio and common stock ratio.

KUnamortized Abandoned Plant and Amortization of Abandoned Plant will be zero until the Commission accepts or approves recovery of the cost of abandoned plant. Company must submit a Section

205 filing to recover the cost of abandoned plant. Any such filing to recover the cost of an abandoned plant item shall be made no later than 180 days after the date that Company formally declares

LUnamortized Regulatory Assets, consisting of all expenses incurred but not included in CWIP prior to the date the rate is charged to customers, is included at line 28

Carrying costs equal to the weighted cost of capital on the balance of the regulatory asset will accrue until the rate is charged to customers

MBalances exclude Asset Retirement Costs

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 1 - Revenue Credit Workpaper* New York Transco LLC

Account 454 - Rent from Electric Property Notes 1 & 3

1 Rent from FERC Form No. 1 -

Account 456 (including 456.1) | Notes 1 & 3 | |

2 Other Electric Revenues (Note 2) 3 Professional Services 4 Revenues from Directly Assigned Transmission Facility Charges (Note 2) 5 Rent or Attachment Fees associated with Transmission Facilities | | - - - - |

6 Total Revenue Credits | Sum lines 2-5 + line 1 | - |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Note 1

Note 2

All revenues booked to Account 454 that are derived from cost items classified as transmission-related will be included as a revenue credit. All revenues booked to Account 456 (includes 456.1) that are derived from cost items classified as transmission-related, and are not derived from rates under this transmission formula rate will be included as a revenue credit. Work papers will be included to properly classify revenues booked to these accounts to the transmission function. A breakdown of all Account 454 revenues by subaccount will be provided below, and will be used to derive the proper calculation of revenue credits. A breakdown of all Account 456 revenues by subaccount and customer will be provided and tabulated below, and will be used to develop the proper calculation of revenue credits.

If the facilities associated with the revenues are not included in the formula, the revenue is shown below, but not included in the total above and explained in the Attachment 3.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Note 3 Line No. | All Account 454 and 456 Revenues must be itemized below | |

1 | Account 456 | TOTAL | NY-ISO | Other 1 | Other 2 |

1a … 1x | Transmission Service Trans. Fac. Charge | - - - | - - | - - | - - |

2 | Trans Studies | - | - | - | - |

3 | Total | - | - | - | - |

4 | Less: | | | | |

5 | Revenue for Demands in Divisor | - | - | - | - |

6 | Sub Total Revenue Credit | ---- |

7 | Prior Period Adjustments | ---- |

8 | Total | |

9 | Account 454 | $ |

9a | Joint pole attachments - telephone | - |

9b | Joint pole attachments - cable | - |

9c | Underground rentals | - |

9d | Transmission tower wireless rentals | - |

9e | Misc non-transmission rentals | - |

9f | | - |

9g | | - |

… | | |

9x | | - |

10 | Total | - |

| | | | | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 2 - Cost Support

New York Transco LLC

Plant in Service Worksheet

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions |

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 | Calculation of Transmission Plant In Service SourceYearBalance |

December p206.58.b January company records February company records March company records April company records May company records June company records July company records August company records September company records October company records November company records December p207.58.g | -- -- -- -- -- -- -- -- -- -- -- -- -- |

Transmission Plant In Service(sum lines 2-14) /13- Calculation of Distribution Plant In Service Source |

December p206.75.b January company records February company records March company records April company records May company records June company records July company records August company records September company records October company records November company records December p207.75.g | -- -- -- -- -- -- -- -- -- -- -- -- -- |

Distribution Plant In Service(sum lines 17-29) /13- |

| | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

61 | Calculation of Production Plant In Service | Source | |

62 | December | p204.46b | -- |

63 | January | company records | -- |

64 | February | company records | -- |

65 | March | company records | -- |

66 | April | company records | -- |

67 | May | company records | -- |

68 | June | company records | -- |

69 | July | company records | -- |

70 | August | company records | -- |

71 | September | company records | -- |

72 | October | company records | -- |

73 | November | company records | -- |

74 | December | p205.46.g | -- |

75 | Production Plant In Service | (sum lines 62-74) /13 | - |

76 | Total Plant In Service | (sum lines 15, 30, 45, 60, & 75) | - |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Accumulated Depreciation Worksheet

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

77 | Calculation of Transmission Accumulated Depreciation | Source | Year | Balance |

78 | December | Prior year p219.25.b | | -- |

79 | January | company records | | -- |

80 | February | company records | | -- |

81 | March | company records | | -- |

82 | April | company records | | -- |

83 | May | company records | | -- |

84 | June | company records | | -- |

85 | July | company records | | -- |

86 | August | company records | | -- |

87 | September | company records | | -- |

88 | October | company records | | -- |

89 | November | company records | | -- |

90 | December | p219.25.b | | -- |

91 | Transmission Accumulated Depreciation | (sum lines 78-90) /13 | | - |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 | Calculation of General Accumulated Depreciation Source |

December Prior year p219.28.b January company records February company records March company records April company records May company records June company records July company records August company records September company records October company records November company records December p219.28.b | -- -- -- -- -- -- -- -- -- -- -- -- -- |

Accumulated General Depreciation(sum lines 123 & 135) /2- Calculation of Production Accumulated Depreciation Source |

Decemberp219.20:24.b (prior year) January company records February company records March company records April company records May company records June company records July company records August company records September company records October company records November company records Decemberp219.20 thru 219.24.b | -- -- -- -- -- -- -- -- -- -- -- -- -- |

Production Accumulated Depreciation(sum lines 138-150) /13- Total Accumulated Depreciation (sum lines 91, 106, 121, 136, & 151)- |

| | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

ADJUSTMENTS TO RATE BASE (Note A) Attachment 3 - Cost Support

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions Details

Beginning of Year End of Year Average Balance

153 Account No. 255 (enter negative) 267.8.h - - -

154 Unamortized Abandoned Plant Per FERC Order - - -

(recovery of abandoned plant requires a FERC order approving the amount and recovery period)

155 Amortization of Abandoned Plant -

156 Prepayments (Account 165)

(Prepayments exclude Prepaid Pension Assets) Year Balance

157 December 111.57.d - -

158 January company records - -

159 February company records - -

160 March company records - -

161 April company records - -

162 May company records - -

163 June company records - -

164 July company records - -

165 August company records - -

166 September company records - -

167 October company records - -

168 November company records - -

169 December 111.57.c - -

170 Prepayments (sum lines 157-169) /13 -

171 Calculation of Transmission CWIP Source Year Non-incentive projects Incentive projects Total

172 December 216.b (prior Year) - - - -

173 January company records - - - -

174 February company records - - - -

175 March company records - - - -

176 April company records - - - -

177 May company records - - - -

178 June company records - - - -

179 July company records - - - -

180 August company records - - - -

181 September company records - - - -

182 October company records - - - -

183 November company records - - - -

184 December 216.b - - - -

185 Transmission CWIP (sum lines 172-184) /13 - - -

LAND HELD FOR FUTURE USE

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions | Beg of year End of Year Average Details |

186 LAND HELD FOR FUTURE USE p214 Total Non-transmission Related Transmission Related | - - - - - - | - - |

| | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Reserves

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

187 List of all reserves: Amount

Enter 1 if Customer

Funded, O if not

Allocation (Plant or

Labor Allocator) Amount Allocated

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Reserve 1 - - - Reserve 2 - - - Reserve 3

Reserve 4

…

… - - - Total - -

The Formula Rate shall include a credit to rate base for all funded and unfunded reserves (i.e. , those for which the funds collected have not been set aside in escrow and the earnings thereon included in the reserve fund) that are funded by customers and for which the associated accrued costs are recoverable under the Formula Rate. Company will include a spreadsheet

(to be included in the Formula Rate template) each year as part of the Annual Update that lists the reserves and indicates which ones meet the test for crediting to rate base.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

EPRI Dues Cost Support

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions Details

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Allocated General & Common Expenses

EPRI Dues EPRI Dues

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

188 EPRI Dues p353._.f (enter FN1 line #)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Regulatory Expense Related to Transmission Cost Support

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Form 1 Amount

Transmission

Related Other

Details*

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Directly Assigned A&G

189 Regulatory Commission Exp Account 928 p323.189.b - - -

* insert case specific detail and associated assignments here

Multi-state Workpaper

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions | New York State 2 State 3 State 4 State 5 Weighed Average |

Income Tax Rates 190 SIT=State Income Tax Rate or Composite | |

| - |

- |

Multiple state rates are weighted based on the state apportionment factors on the state income tax returns and the number of days in the year that the rates are effective (see Note F) |

| | |

Safety Related and Education and Out Reach Cost Support

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Directly Assigned A&G

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Form 1 Amount

Safety Related, Education, Siting

& Outreach

Related Other

Details

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

191 General Advertising Exp Account 930.1 p323.191.b -

Excluded Plant Cost Support

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions | Excluded Transmission Facilities Description of the Facilities |

Adjustment to Remove Revenue Requirements Associated with Excluded Transmission Facilities 192 Excluded Transmission Facilities | - General Description of the Facilities Add more lines if necessary |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Materials & Supplies

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Note: for the projection, the prior year's actual balances will be used

Stores Expense

Undistributed

Transmission Materials & Supplies

Construction

Materials & Supplies Total

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Form No.1 page p227.16 p227.8 p227.5

193 December Column b - - - -

194 January - - - -

195 February - - - -

196 March - - - -

197 April - - - -

198 May - - - -

199 June - - - -

200 July - - - -

201 August - - - -

202 September - - - -

203 October - - - -

204 November - - - -

205 December Column c - - - -

206 Average -

Regulatory Asset

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions |

207 Beginning Balance of Regulatory Asset 208 Months remaining in Amortization Period | Project Name Project Name Project Name | Total Uncapitalized costs as of date the rates become effective As approved by FERC |

- - - - - - |

All amortizations of the Regulatory Asset are to be booked to Account 566 over a 5 year period beginning on the first month that the revenue 209 Monthly Amortization to Account 566 (line 207 / line 208) - - - - requirement for the project is assessed 210 Months in Year to be amortized - - - Number of months rates are in effect during the calendar year 210a Annual Amortization (line 209 * line 210) - - - - 211 Ending Balance of Regulatory Asset (line 207 - line 209 * 210) - - - Enter docket nos. for orders authorizing recovery here: 212 Average Balance of Regulatory Asset (line 207 + line 211)/2 - - - - Docket Number Amortization period |

| | | |

| |

| |

| | | | | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Capital Structure

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

213 Monthly Balances for Capital Structure Year Debt Preferred Stock Common Stock Total Capitalization

214

215

216

217

218

219

220

221

222

223

224

225

226

227 Average - - - -

Debt is equal to 112.18c less 112.19c plus 112.20c plus 112.21c, recognizing that 112.19c is entered into the Form 1 as a negative number and shall remain negative (i.e., it is not a double minus in the formula that mathematically would lead to adding in line 112.19c) so that Reacquired Bonds (Account 222) are subtracted from other long term debt outstanding and that Line 112.20c may contain both short term and long term indebtedness to affiliates and therefore any short term affiliate debt shall be removed from 112.20c before adding it into the above long term debt balance formula in the formula rate.

Preferred Stock is equal to 112.3c less any Preferred Treasury Stock plus any Preferred Additional Paid-in-Capital, recognizing that if there is any Preferred Treasury Stock or Preferred Additional Paid-in-Capital, then the respective amounts shall be appropriately disclosed in a footnote to the capital structure cost support in the formula rate template.

Common Equity is equal to 112.16c less 112.3c less 112.12c less 112.15c, recognizing that line 112.15c may be a positive or negative number and if it is positive, it shall be subtracted in the formula, and if it is entered as a negative in the Form 1, it shall be added (a double minus sign when subtracting a negative number) in the formula.

The cost of long-term debt for a Rate Year will be the sum of the interest expense and cost of issuances divided by the 13-month average long-term debt balance for the Rate Year. The cost of long-term debt issuances shall include long-term interest expense amounts recorded in the following FERC accounts:

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

228 Account 427

229 plus: Account 428

230 plus: Account 428.1

231 less: Account 429

232 less: Account 429.1

233 plus: Account 430

Interest on Long-Term Debt (limited solely to interest expense for long-term debt reported in Accounts 221-224) (FF1,

117/62/c)

Amortization of Debt Discount and Expense (FF1, 117/63/c) Amortization of Loss on Reacquired Debt (FF1, 117/64/c) Amortization of Premium on Debt (FF1, 117/65/c)

Amortization of Gain on ReacquiredpDebt (FF1, 117/66/c) y

the expense associated with long-term debt recorded in Account

223.

Amount

-

-

-

-

-

-

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

234 Total -

Interest expenses not directly related to the long-term bond issuances included in the capital structure will be excluded.

The cost of preferred stock will be preferred stock dividends (booked in FERC Account 437) divided by the average preferred stock balance for the rate year.

235 Preferred Dividends in Account 437 -

236 13 Month average balance of Preferred Stock -

237 Cost of Preferred Stock -

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

PBOPs

Appendix A Line #s, Descriptions, Notes, Form 1 Page #s and Instructions

Details

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

238 Calculation of PBOP Expenses

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

239 ConEd

240 Total PBOP expenses

241 Labor dollars

242 Cost per labor dollar

$ 22,000,000

$ 1,394,368,000

$ 0.0158

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

243 labor (labor not capitalized) current year -

244 PBOP Expense for current year -

245 PBOP Expense in Account 926 for current year -

246 PBOP Adjustment for Appendix A, Line 54 -

247 Lines 240-242 cannot change absent approval or acceptance by FERC in a separate proceeding.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

247 NiMo

248 Total PBOP expenses

249 Labor dollars

250 Cost per labor dollar

$ 72,221,472

$ 438,541,722

$ 0.1647

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

251 labor (labor not capitalized) current year -

252 PBOP Expense for current year -

253 PBOP Expense in Account 926 for current year -

254 PBOP Adjustment for Appendix A, Line 54 -

255 Lines 248-250 cannot change absent approval or acceptance by FERC in a separate proceeding.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

256 NYSEG

257 Total PBOP expenses

258 Labor dollars

259 Cost per labor dollar

$ 2,974,219

$ 171,780,082

$ 0.0173

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

260 labor (labor not capitalized) current year -

261 PBOP Expense for current year -

262 PBOP Expense in Account 926 for current year -

263 PBOP Adjustment for Appendix A, Line 54 -

264 Lines 257-259 cannot change absent approval or acceptance by FERC in a separate proceeding.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

265 RGE

266 Total PBOP expenses

267 Labor dollars

268 Cost per labor dollar

$ 3,411,650

$ 66,576,513

$ 0.0512

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

269 labor (labor not capitalized) current year -

270 PBOP Expense for current year -

271 PBOP Expense in Account 926 for current year -

272 PBOP Adjustment for Appendix A, Line 54 -

273 Lines 266-268 cannot change absent approval or acceptance by FERC in a separate proceeding.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

274 CHG&E

275 Total PBOP expenses $432,757

276 Labor dollars 45,945,646

277 Cost per labor dollar $0.009

278 labor (labor not capitalized) current year -

279 PBOP Expense for current year -

280 PBOP Expense in Account 926 for current year -

281 PBOP Adjustment for Appendix A, Line 54 -

282 Lines 275-277 cannot change absent approval or acceptance by FERC in a separate proceeding.

283 New York Transco LLC

284 Total PBOP expenses $ -

285 Labor dollars $ -

286 Cost per labor dollar $0.000

287 labor (labor not capitalized) current year -

288 PBOP Expense for current year -

289 PBOP Expense in Account 926 for current year -

290 PBOP Adjustment for Appendix A, Line 54 -

291 Lines 284-286 cannot change absent approval or acceptance by FERC in a separate proceeding.

292 PBOP expense adjustment (sum lines 246, 263, 254, 272, 281, & 290) -

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Incentive ROE and 60/40 Project WorksheetRate Formula TemplateFor the 12 months ended 12/31/2012

Attachment 4Utilizing Attachment O Data

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Base ROE and Income Taxes Carrying Charge

New York Transco LLC

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

1 | Rate Base | | | - |

2 | Base Return | | | $ |

| | Cost $%(Note P) | | Weighted |

3 | Long Term Debt | --- | | - |

4 | Preferred Stock | --- | | - |

5 | Common Stock | --10.60% | | - |

6 | Total (sum lines 3-5) | - | | - |

7 | Return multiplied by Rate Base (line 1 * line 6) | | | - |

8 | INCOME TAXES | | | |

9 | T=1 - {[(1 - SIT) * (1 - FIT)] / (1 - SIT * FIT * p)} = | - | | |

10 | CIT=(T/1-T) * (1-(WCLTD/R)) = | - | | |

11 | where WCLTD=(line 3) and R= (line 6) | | | |

12 | and FIT, SIT & p are as given in footnote F on Appendix A. | | | |

13 | 1 / (1 - T) = (T from line 9) | - | | |

14 | Amortized Investment Tax Credit (266.8f) (enter negative) | - | |

15 | | | |

16 | Income Tax Calculation = line 10 * line 7 | | - |

17 | ITC adjustment (line 13 * line 14) and line 17 allocated on NP allocator | -NP | -- |

18 | Total Income Taxes(line 16 plus line 17) | - | - |

| | | | | |

19 | Base Return and Income Taxes | Sum lines 7 and 18 | | - |

20 | Rate Base | Line 1 | | - |

21 | Return and Income Taxes at Base ROE | Line 19 / line 20 | #DIV/0! | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Incentive ROE and Income Taxes Carrying ChargeAttachment 4

22 | Rate Base | | | - |

23 | 100 Basis Point Incentive Return | | | $ |

| | Cost $%(Note P) | | Weighted |

24 | Long Term Debt | --- | | - |

25 | Preferred Stock | --- | | - |

26 | Common Stock Including 100 basis points | --11.60% | | - |

27 | Total (sum lines 28-30) | - | | - |

28 | 100 Basis Point Incentive Return multiplied by Rate Base (line 26 * line 31) | | | - |

29 | INCOME TAXES | | | |

30 | T=1 - {[(1 - SIT) * (1 - FIT)] / (1 - SIT * FIT * p)} = | - | | |

31 | CIT=(T/1-T) * (1-(WCLTD/R)) = | - | | |

32 | where WCLTD=(line 24) and R= (line 27) | | | |

33 | and FIT, SIT & p are as given in footnote on Appendix A. | | | |

34 | 1 / (1 - T) = (T from line 30) | - | | |

35 | Amortized Investment Tax Credit (266.8f) (enter negative) | - | | |

36 | Income Tax Calculation = line 31 * line 28 | | - |

37 | ITC adjustment (line 34 * line 35) and line 41 allocated on NP allocator | -NP | -- |

38 | Total Income Taxes(line 36 plus line 37) | - | - |

39 | Return and Income Taxes with 100 basis point increase in ROE | Sum lines 32and 42 | - |

40 | Rate Base | Line 1 | - |

41 | Return and Income Taxes with 100 basis point increase in ROE | Line 39 / line 40 | - |

42 | Difference in Return and Income Taxes between Base ROE and 100 Basis Point Incentive | Line 41 - Line 21 | - |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 4

Revenue Requirement per project including incentives

Base Carrying ChargeLine 102 Appendix A0.00%

(a)(b)(c)(d)(e)(f)(g)(h)(i)(j)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

DescriptionAmount

ROE Authorized

by FERCROE Base

Incentive % Authorized by

FERCLine 42

Col (e) / .01 x

Col (f)

Incentive $ (Col

(b) x Col (g)

Base Revenues (Base Carrying Charge x Col (b)

Total Revenues

(Col (h) + Col (i)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

| 43 | ---10.60% | ------ |

44 | ---10.60% | ------ |

45 | 10.60% | |

46 | 10.60% | |

47 | 10.60% | |

48 | 10.60% | |

49 | 10.60% | |

50 | 10.60% | |

51 | 10.60% | |

52 | 10.60% | |

53 | 10.60% | |

54 | 10.60% | |

55 | 10.60% | |

56 | 10.60% | |

57 | 10.60% | |

57a | | 10.60% | |

57b | | 10.60% | |

… | | 10.60% | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

58 Total

Check Sum Apendix A Line 3

Difference (must be zero)

$-$

-$-

$-

$-

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Note:

To the extent that the stated incenitive return is limited by the top of the range of reasonableness, the returns on equity applied to the various projects and facilities shall not produce an overall company return exceeding the top of the range of reasonableness.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

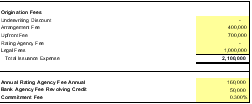

Attachment 5 - Financing Costs for Long Term Debt using the Internal Rate of Return Methodology

New York Transco LLC Estimated

Assumes financing will be a 5 year loan with Origination Fees of $2.1 million and a Commitments Fee of 0.3% on the undrawn principal. Consistent with GAAP, the Origination Fees and Commitments Fees will be amortized using the standard Internal Rate of Return formula below.

Each year, the amounts withdrawn, the interest paid in the year, Origination Fees, Commitments Fees, and total loan amount will be updated on this attachment.

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

1 Total Loan Amount

$ 200,000,000

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

2 Internal Rate of Return1 5.634%

3 Based on following Financial Formula2:

4 NPV = 0 =

Table 1

5

6

7

8

9

10

11

12

13

Table 2

14

15

16

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Table 3

(A)(B)( C)(D)(E)(F)(G)(H)(I)

Principal

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

17Year

Capital

Expenditures (

$000's)

Drawn In Quarter ($000's)

Principal Drawn

To Date ($000's)

Interest & Principal ($000's)

1/4 * Interest Rate from Line 16 x

Origination

Fees ($000's)

Commitment & Utilization Fee ($000's)

Net Cash Flows

($000's)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Col. E prior

Input in first Qtr of Lines 11 - 12 x (Line 1

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Cumulative Col. D

quarter

Loan

less Col. E prior quarter)(D-F-G-H)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

18 | |

19 | 3/31/2014 | Q3 | 19,350 | 7,740 | 7,740 | | 2,100 | | 5,640 |

20 | 6/30/2014 | Q4 | 19,350 | 7,740 | 15,480 | 56 | | 354 | 7,330 |

21 | 9/30/2014 | Q1 | 19,350 | 7,740 | 23,220 | 113 | | 138 | 7,489 |

22 | 12/31/2014 | Q2 | 19,350 | 7,740 | 30,960 | 169 | | 133 | 7,439 |

23 | 3/31/2015 | Q3 | 24,775 | 9,910 | 40,870 | 220 | | 127 | 9,563 |

24 | 6/30/2015 | Q4 | 24,775 | 9,910 | 50,780 | 335 | | 329 | 9,246 |

25 | 9/30/2015 | Q1 | 24,775 | 9,910 | 60,690 | 420 | | 112 | 9,378 |

26 | 12/31/2015 | Q2 | 24,775 | 9,910 | 70,600 | 502 | | 104 | 9,303 |

27 | 3/31/2016 | Q3 | 23,950 | 9,580 | 80,180 | 578 | | 97 | 8,905 |

28 | 6/30/2016 | Q4 | 23,950 | 9,580 | 89,760 | 770 | | 300 | 8,511 |

29 | 9/30/2016 | Q1 | 23,950 | 9,580 | 99,340 | 871 | | 83 | 8,626 |

30 | 12/31/2016 | Q2 | 23,950 | 9,580 | 108,920 | 964 | | 75 | 8,540 |

31 | 3/31/2017 | Q3 | 23,575 | 9,430 | 118,350 | 1,034 | | 68 | 8,328 |

32 | 6/30/2017 | Q4 | 23,575 | 9,430 | 127,780 | 1,292 | | 271 | 7,866 |

33 | 9/30/2017 | Q1 | 23,575 | 9,430 | 137,210 | 1,411 | | 54 | 7,965 |

34 | 12/31/2017 | Q2 | 23,575 | 9,430 | 146,640 | 1,515 | | 47 | 7,868 |

35 | 3/31/2018 | Q3 | - | - | 146,640 | 148,224 | | 40 | (148,264) |

36 | 6/30/2018 | Q4 | - | - | - | - | | - | - |

37 | 9/30/2018 | Q1 | - | - | - | - | | - | - |

38 | | | | | | | | | |

39 | | | | | | | | | |

40 | | | | | | | | | |

41 | | | | | | | | | |

42 | | | | | | | | | |

43 | | | | | | | | | |

44 | | | | | | | | | |

45 | | | | | | | | | |

| | | | | | | | | |

Notes 1. During the contruction period, the IRR is the Debt Cost shown on Line 91 of Appendix A after debt is issued and the Interest Rate in Table 2 prior to debt being issued."

2. The IRR is a discount rate that makes the net present value of a series of cash flows equal to zero. The IRR equation is shown on line 4.

N is the last quarter the loan would be outstanding t is each quarter

Ct is the cash flow (Tabel 3, Col.I in each quarter)

alternatively the equation can be written as 0 = C0 + C1/(1+IRR) + C2/(1+IRR)2 + C3/(1+IRR)3 + . . . +Cn/(1+IRR)n and solved for IRR

3. Line 1 relfects the loan amount, the maximum amount that can be drawn on

4. Lines 5 throught 13 include the fees associated with the loan. They are estimated based on current bank condition and are updated with the actual fees once the actual fees are known.

5. Line 14 is the average daily Libor monthly interest rate for the prior month for the estimate and the actual daily Libor monthly interest rate for the prior year for the True-Up.

6. Table 3, Col. C reflect the capital expenditures in each quarter

7. Table 3, Col. D reflect the amount of the load that is drawn down in the quarter

8. Table 3, Col. G is the total origination fees in line 10 and is input in the first quarter that a portion of the load in drawn

9. Table 3, Col. H is calculated as follows: A x (B +C)

A. Loan amount in line 1 less the amount drawn down in the prior quarter

B. Annual dollar amount fees on lines 11 throught 13 divided by 4

C. Percentage dollar amounts divided by 1000

10. The inputs shall be estimated based on the current market conditions and is subject to true up for all inputs , e.g., fees, interest rates, spread, and Table 3 once the amounts are known

11. The interest rate in line 16 for the corresponding year is used in Appendix A line 91 until the project financing is obtained. Thereafter the interst rate in line 2 is used on Appendix A line 91

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6a - Accumulated Deferred Income Taxes (ADIT) Worksheet (Beginning of Year) Beginning of Year

Transmission Plant Labor Total

Item 1 | ADIT- 282 | Related | Related - | Related - | Plant & Labor Related - | From Acct. 282 total, below |

2 | ADIT-283 | | - | - | - | From Acct. 283 total, below |

3 | ADIT-190 | | - | - | - | From Acct. 190 total, below |

4 | Subtotal | | - | - | - | |

5 | Wages & Salary Allocator | | | | - | |

6 | NP | | | - | | |

7 | Beginning of Year | | - | - | - - | |

8 | End of year from Attachment 6b, line 7 | | - | - | - - | |

9 | Average of Beginning of Year and End of Year ((7 +8)/2) | | - | - | - - | Enter as negative Appendix A, line 24. |

In filling out this attachment, a full and complete description of each item and justification for the allocation to Columns B-F and each separate ADIT item will be listed,

dissimilar items with amounts exceeding $100,000 will be listed separately. For ADIT directly related to project depreciation or CWIP, the balance must shown in a separate column for each project.

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p234 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | | | | | | |

Less FASB 106 Above if not separately removed | | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 190:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6a - Accumulated Deferred Income Taxes (ADIT) Worksheet (Beginning of Year) Beginning of Year

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p275 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | | | | - | | |

Less FASB 106 Above if not separately removed | | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 282:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6a - Accumulated Deferred Income Taxes (ADIT) Worksheet (Beginning of Year) Beginning of Year

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p277 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | - | | | - | | |

Less FASB 106 Above if not separately removed | - | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 283:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6b - Accumulated Deferred Income Taxes (ADIT) Worksheet (End of Year)

End of Year

| Transmission | Plant | Labor | Total |

Line | Related | Related | Related | Plant & Labor Related |

1 ADIT- 282---From Acct. 282 total, below

2 ADIT-283---From Acct. 283 total, below

3 ADIT-190---From Acct. 190 total, below

4 Subtotal---

5 Wages & Salary Allocator-

6 NP-

7 End of Year ADIT----

In filling out this attachment, a full and complete description of each item and justification for the allocation to Columns B-F and each separate ADIT item will be listed, dissimilar items with amounts exceeding $100,000 will be listed separately.

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p234 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | | | | | | |

Less FASB 106 Above if not separately removed | | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 190:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6b - Accumulated Deferred Income Taxes (ADIT) Worksheet (End of Year)

End of Year

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p275 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | | | | - | | |

Less FASB 106 Above if not separately removed | | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 282:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

New York Transco LLC

Attachment 6b - Accumulated Deferred Income Taxes (ADIT) Worksheet (End of Year)

End of Year

G

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Subtotal - p277 | - | - | - | - | - | |

Less FASB 109 Above if not separately removed | - | | | - | | |

Less FASB 106 Above if not separately removed | - | | | | | |

Total | - | - | - | - | - | |

Instructions for Account 283:

1. ADIT items related only to Non-Electric Operations (e.g., Gas, Water, Sewer) or Production are directly assigned to Column C

2. ADIT items related only to Transmission are directly assigned to Column D

3. ADIT items related to Plant and not in Columns C & D are included in Column E

4. ADIT items related to labor and not in Columns C & D are included in Column F

5. Deferred income taxes arise when items are included in taxable income in different periods than they are included in rates, therefore if the item giving rise to the ADIT is not included in the formula, the associated ADIT amount shall be excluded

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 7 - Example of True-Up Calculation

New York Transco LLC

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

20132013

Actual Revenue

Over (Under)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Revenue Requirement Billed*

Requirement

Recovery

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

$2,000,000Less$2,120,000Equals($120,000)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Interest Rate on Amount of Refunds or Surcharges

0.5500%

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

An over or under collection will be recovered prorata over year collected, held for one year and returned prorata over next year. If the first year is a partial year, the true-up (over or under recovery per month and interest calculation) will reflect only the number of months for which the rate was charged.

Calculation of Interest | | | | | Monthly | |

January | Year 2013 | (10,000) | 0.5500% | 12 | | 660 | | 10,660 |

February | Year 2013 | (10,000) | 0.5500% | 11 | | 605 | | 10,605 |

March | Year 2013 | (10,000) | 0.5500% | 10 | | 550 | | 10,550 |

April | Year 2013 | (10,000) | 0.5500% | 9 | | 495 | | 10,495 |

May | Year 2013 | (10,000) | 0.5500% | 8 | | 440 | | 10,440 |

June | Year 2013 | (10,000) | 0.5500% | 7 | | 385 | | 10,385 |

July | Year 2013 | (10,000) | 0.5500% | 6 | | 330 | | 10,330 |

August | Year 2013 | (10,000) | 0.5500% | 5 | | 275 | | 10,275 |

September | Year 2013 | (10,000) | 0.5500% | 4 | | 220 | | 10,220 |

October | Year 2013 | (10,000) | 0.5500% | 3 | | 165 | | 10,165 |

November | Year 2013 | (10,000) | 0.5500% | 2 | | 110 | | 10,110 |

December | Year 2013 | (10,000) | 0.5500% | 1 | | 55 | | 10,055 |

| | | | | | 4,290 | | 124,290 |

| | | | | Annual | | | |

January through December | Year 2014 | 124,290 | 0.5500% | 12 | | 8,203 | | 132,493 |

Over (Under) Recovery Plus Interest Amortized and Recovered Over 12 MonthsMonthly |

January | Year 2015 | (132,493) | 0.5500% | | | 729 | (11,440) | 121,782 |

February | Year 2015 | (121,782) | 0.5500% | | | 670 | (11,440) | 111,012 |

March | Year 2015 | (111,012) | 0.5500% | | | 611 | (11,440) | 100,183 |

April | Year 2015 | (100,183) | 0.5500% | | | 551 | (11,440) | 89,294 |

May | Year 2015 | (89,294) | 0.5500% | | | 491 | (11,440) | 78,345 |

June | Year 2015 | (78,345) | 0.5500% | | | 431 | (11,440) | 67,337 |

July | Year 2015 | (67,337) | 0.5500% | | | 370 | (11,440) | 56,267 |

August | Year 2015 | (56,267) | 0.5500% | | | 309 | (11,440) | 45,137 |

September | Year 2015 | (45,137) | 0.5500% | | | 248 | (11,440) | 33,945 |

October | Year 2015 | (33,945) | 0.5500% | | | 187 | (11,440) | 22,692 |

November | Year 2015 | (22,692) | 0.5500% | | | 125 | (11,440) | 11,377 |

December | Year 2015 | (11,377) | 0.5500% | | | 63 | (11,440) | (0) |

| | | | | | 4,784 | | |

| | | | | | | | |

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Total Amount of True-Up Adjustment

Less Over (Under) Recovery

Total Interest

$137,277

$(120,000)

$17,277

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

* excluding any true up for prior period

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 7a

True-Up Interest Calculation Page 2

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

FERC Quarterly Interest Rate

Purusant to

35.19 (a)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

1 Qtr 3 (Previous Year) -

2 Qtr 4 (Previous Year) -

3 Qtr 1 (Current Year) -

4 Qtr 2 (Current Year) -

5 Average of the last 4 quarters (Lines 1-4 / 4) -

6 Interest Rate Used for True-up adjustment (Note B) -

7 Monthly Interest Rate for Attachment 7 (Line 6 / 12) -

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Attachment 8 - Hypothetical Example of Final True-Up of Interest Rates and Interest Calculations for the Construction Loan

New York Transco LLC

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

YEAR

Estimated Effective cost of debt used in true up

Final Effective cost of debt for the construction loan:

SUMMARY

Based on Estimated Effective cost of debt

Revenue Requirement

Based on Actual Effective cost of debt

Over (Under) Recovery

Monthly FERC Refund Interest Rate applicable over the ATRR period

Total Amount of Construction Loan Related True-Up to be included in rates (Refund)/Owed

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

20147.18%6.50%

$ 2,500,000.00

$ 2,400,000.00

$ 100,000.00

0.550% $

(148,288.33)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

20156.8%6.50%$5,000,000.00$5,150,000.00

20167.2%6.50%$8,300,000.00$8,200,000.00

20177.3%6.50%$12,300,000.00$12,000,000.00

2018*7.1%6.50%$18,000,000.00$17,900,000.00

2018**6.50%6.50%$25,000,000.00$25,000,000.00

The Hypothetical Example:

* Assumes that the construction loan is retired on December 31, 2018

** Assumes that the contruction loan IRR on Attachment 5 has an effective rate of 6.5%

$ (150,000.00)

$ 100,000.00

$ 300,000.00

$ 100,000.00

$-

0.560% $

0.540% $

0.580% $

0.570% $

$

209,670.43 (131,109.09) (368,656.73) (114,946.28)

(553,329.99)

Effective Date: 4/3/2015 - Docket #: ER15-572-000 - Page 1

NYISO Tariffs --> Open Access Transmission Tariff (OATT) --> 36 OATT Attachment DD - Rules to Allocate the Cost of NY Tra

Calculation of Applicable Interest Expense for each ATRR period

| Hypothetical Monthly | | | | Surcharge (Refund) |

Interest Rate on Amount of Refunds or Surcharges from 35.19a | Over (Under) Recovery Plus Interest | Interest Rate | Months | Calculated Interest | Amortization | Owed |

| | | | | | |

Calculation of Interest for 2014 True-Up Period

An over or under collection will be recovered prorata over 2014, held for 2015, 2016, 2017, 2018, and 2019 and returned prorate over 2020Monthly

January | Year 2014 | - | 0.5500% | 12.00 | - | - |

February | Year 2014 | - | 0.5500% | 11.00 | - | - |

March | Year 2014 | 10,000 | 0.5500% | 10.00 | (550) | (10,550) |

April | Year 2014 | 10,000 | 0.5500% | 9.00 | (495) | (10,495) |

May | Year 2014 | 10,000 | 0.5500% | 8.00 | (440) | (10,440) |

June | Year 2014 | 10,000 | 0.5500% | 7.00 | (385) | (10,385) |

July | Year 2014 | 10,000 | 0.5500% | 6.00 | (330) | (10,330) |

August | Year 2014 | 10,000 | 0.5500% | 5.00 | (275) | (10,275) |

September | Year 2014 | 10,000 | 0.5500% | 4.00 | (220) | (10,220) |

October | Year 2014 | 10,000 | 0.5500% | 3.00 | (165) | (10,165) |

November | Year 2014 | 10,000 | 0.5500% | 2.00 | (110) | (10,110) |

December | Year 2014 | 10,000 | 0.5500% | 1.00 | (55) | (10,055) |

| | | | | (3,025) | (103,025) |

Annual

January through December | Year 2015 | (103,025) | 0.5600% | 12.00 | (6,923) | (109,948) |