UNITED STATES OF AMERICA

BEFORE THE

FEDERAL ENERGY REGULATORY COMMISSION

Joint Technical Conference on New York Markets)&Docket No. AD14-18-000

Infrastructure)

INTRODUCTORY COMMENTS OF STEPHEN G. WHITLEY

PRESIDENT AND CHIEF EXECUTIVE OFFICER

NEW YORK INDEPENDENT SYSTEM OPERATOR, INC.

Good Morning, my name is Stephen G. Whitley. I am President and CEO of the New York

Independent System Operator and have served in that position for the past seven years. Prior to joining NYISO, I served as Chief Operating Officer at ISO-NE for seven years and before that I held various senior positions at the Tennessee Valley Authority for over twenty years. Thank you for the opportunity to participate in today’s technical conference.

The topic for today’s discussion is not without controversy. So, at the outset, let me say that I see today’s conference as an opportunity for the FERC, the PSC, and New York’s stakeholders to continue the collaboration that started in the 1990s when the NYISO was first conceived and formed to benefit New Yorkers. I look forward to a constructive dialogue that will help the

NYISO provide additional benefits to New York’s electric customers.

1

I have been involved in the operation of wholesale electricity markets for 15 years and I can

confidently say that the NYISO’s market design, which includes both energy and capacity, is

working well to achieve the goals envisioned by the New York PSC in its Competitive

Opportunities Case and by FERC in its orders approving the ISO-administered markets.

First, NYISO’s locational energy and capacity price signals have gotten generation built and

gotten it built in the right places. We have already seen significant new entry in southeast New York, the State’s load center. My experience in New England was much different because there we initially lacked adequate locational price signals. There I saw developers make very

inefficient decisions about where to site power plants.

Since the inception of the NYISO, most of the new entrants have been clean, efficient combined cycle units, which has contributed to the New York generation fleet’s improved heat rate and reduced harmful emissions. Contributing to this positive environmental trend is the fact that 6,000 MW of older generation has retired or ceased operation since the NYISO’s start-up. Old, dirty, and inefficient units will ultimately go away under competition.

The NYISO’s competitive markets have also given generators the incentive to always be

available to operate. New York’s generators have much higher availability and capacity factors

than they did under the cost-of-service regime. These attributes are obviously good for

reliability.

2

For the most part, the units are now owned and operated by merchant developers, which has shifted the risk of investments away from end-users who have historically borne much of the cost of stranded investments. If a power plant proves uneconomic under today’s model,

ratepayers are protected from having to pay for that project.

In an effort to send accurate price signals the NYISO has worked hard to get the marginal units

to set energy prices and most recently we have improved shortage and scarcity pricing rules to

take the pressure off of the amount of capacity market revenues needed. Sending accurate

price signals minimizes out-of-merit dispatch and uplift costs that loads cannot hedge. When I

started at the NYISO in 2008, we had a major uplift challenge and the end users, particularly

commercial and industrial customers, let me know about it at a high decibel level. I am proud

to say that we have successfully addressed that issue and now experience very low uplift in

New York.

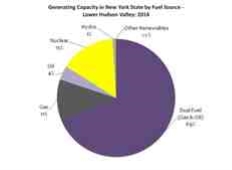

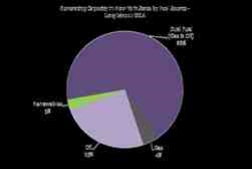

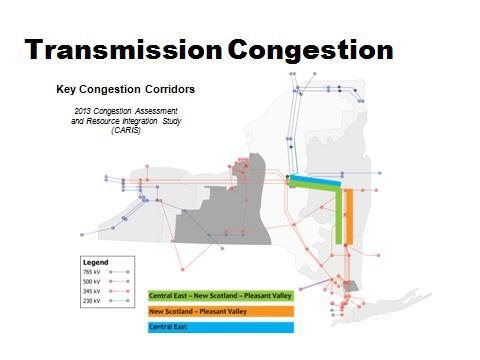

But we have had some major challenges during my tenure. First, it is important to understand that we have a highly constrained transmission system that cannot adequately deliver power from upstate New York into southeast New York, particularly the lower Hudson Valley and New York City. We have abundant generating resources in western and northern New York but lack the transmission to get it downstate.

3

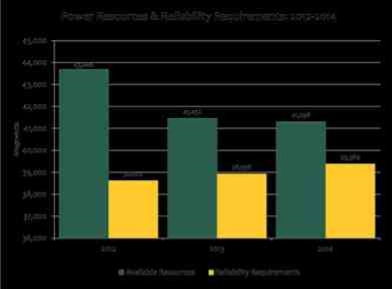

Second, although we have had a lot of new capacity entry in New York over the past 15 years, between 2012 and 2014 we saw our supply resources above the minimum requirement level shrink from 5,000 MW to only 1,900 MW.

Generation: Narrowing Margins

2012 power resources were 5,000+ MW

above reliability requirements

2014 surplus is slightly above 1,900 MW

This reduction is not cause for alarm. It is largely the result of the interplay of competitive forces. Effective NYISO market and planning mechanisms are already in place to preserve reliability. For example, during the summer of 2013, we had to call on demand response five times to address a period of prolonged high temperatures.

A long-standing transmission constraint and shrinking resource margins caused us to create a

new capacity zone in the lower Hudson Valley and New York City. A locational price signal was

needed to attract new generation and retain existing units needed to maintain reliability. The

new capacity zone has caused a great deal of controversy - and litigation. But the alternative -

risking reliability - was unacceptable to the NYISO as the entity entrusted with keeping the

lights on in New York.

4

Despite the controversy, the new capacity zone is working. Two major generating facilities -

Danskammer and Bowline - are in the process of returning to service based on strong market signals. So we are successfully retaining units needed for reliability. And as these units go back into service, wholesale capacity prices are expected to go down. Emilie Nelson, the NYISO’s Vice President for Market Operations, will describe this in more detail.

Does this mean we do not need transmission? Absolutely not. Generation alone cannot solve our problems. New York needs new investment in both transmission and generation to

maintain system reliability. We need transmission for several reasons.

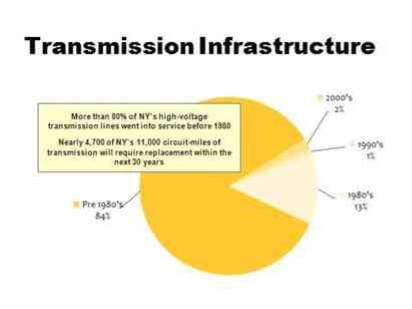

First, we have an aging transmission grid that needs to be upgraded. Although we are meeting minimum reliability standards, new transmission will enhance reliability and provide

operational flexibility.

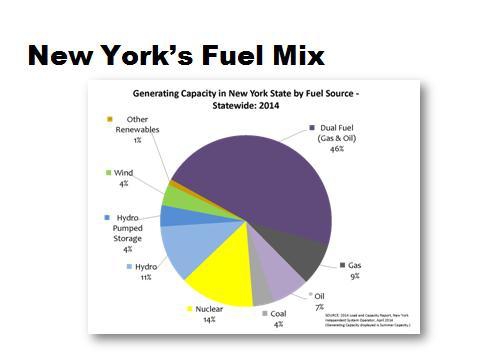

Second, there is a great deal of concern about fuel diversity. Last winter we successfully

operated the system through the Polar Vortex events in large part because we were able to

switch to oil when gas supplies got tight. We know we cannot depend solely on natural gas to

fuel our power plants. The good news is that we already have a very diverse fleet of resources

in New York State. In northern and western New York we have abundant non-gas-fired

resources including hydro, wind, and nuclear. But we cannot deliver that power to the load

center.

5

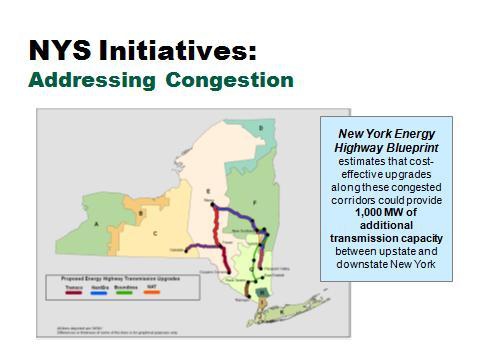

Finally, building new transmission to optimize our use of resources will help improve our air quality and yield environmental benefits for New York. The Governor’s Energy Highway initiatives and the PSC’s AC transmission proceeding can help solve the problem of overreliance on natural gas. Emilie Nelson will talk about our successes so far.

My view is that New York already has a solid market design, but the NYISO is committed to making it better with all of your support and input.

Emilie is going to give you some more detail about how our capacity market works, hurdles we are working to overcome, capacity and energy market initiatives we are working on, and how we are preparing for extreme weather like we saw last winter.

Then David Patton, the NYISO’s Independent Market Monitor, will provide his assessment of how the New York capacity market is working and things we can do to improve it.

Thank you.

7